Share on Facebook

Share on Facebook Share on X

Share on X Share by Email

Share by Email Share on Google Classroom

Share on Google Classroom

Credit Unions

Credit Unions, financial co-operatives that provide deposit, chequing and lending services to the member owners. Owned locally and operated under provincial jurisdiction, they jointly own provincial central organizations. Robert Owen began a consumer co-operative among unemployed weavers of Rochdale, England, in 1844, and co-operative principles for buying and selling were applied to borrowing and lending in an experiment in Germany. The original credit unions were not only mutual self-help societies but a strong moral and spiritual force.

The first successful credit union in Canada, a Caisse Populaire, was started at Lévis, Qué, in 1900 by Alphonse Desjardins. Attempts in the 1920s to establish credit unions in English-speaking areas in Ontario and the West did not succeed. In the 1930s the organizers of the Antigonish Movement associated themselves with the (American) Credit Union National Association and established a credit union in Broad Cove (1932). Credit unions grew rapidly in Atlantic Canada during the Great Depression, and by the early 1940s they were being established across English Canada. The CCF government in Saskatchewan specifically encouraged their formation.

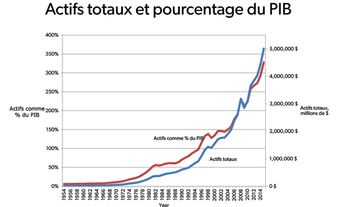

To facilitate the exchange of savings and to help local credit unions become more efficient, credit-union leaders in all the English-speaking provinces organized provincial centrals (called co-operative credit societies or credit-union leagues), which distinguished them in name if not in substance from caisses populaires. In 1953 some of the centrals, along with other nonfinancial co-operatives, organized the Canadian Co-operative Credit Society, a national organization used primarily to transfer funds among the centrals. During the 1950s and 1960s credit unions, which are generally smaller than caisses populaires, grew rapidly, largely through using member savings to provide mortgages and short-term loans. They were able to compete effectively with banks because of low administrative costs, inexpensive premises and convenient service hours. In the same period, they gradually acquired the legal right to offer most of the financial services, such as chequing, provided by banks.

In many areas, particularly on the Prairies and in BC, anyone in a geographic area could join - not just members of a specific trades union or of specific professional or church organizations. Growth continued through to the early 1980s, largely because of the demand for mortgages (caisses populaires have, on the other hand, reduced the proportion of their funds invested in securities and mortgages).

The recession of the early 1980s was particularly hard on all western credit-granting institutions, and the credit unions were no exception. The general collapse in property values, attendant upon the recession, meant that asset values of credit unions declined correspondingly. The inevitable liquidity crisis meant that provincial government assistance was necessary in order to maintain solvency.